China’s economy lost momentum in the second quarter of 2026, with weaker domestic demand offsetting the benefits of resilient exports. The slowdown may be closely watched by Australian investors given China’s importance as Australia’s largest trading partner and a major consumer of Australian commodities.

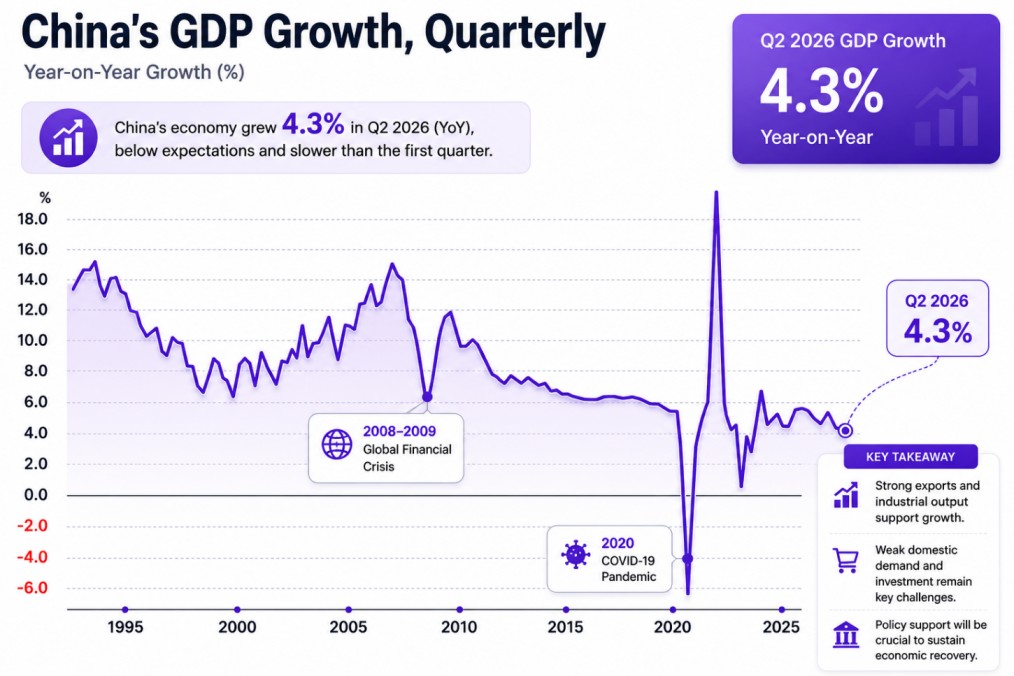

According to data released by China’s National Bureau of Statistics, gross domestic product (GDP) expanded by 4.3% year-on-year during the April–June quarter. The result came below market expectations of 4.5% and marked a slowdown from the 5.0% growth recorded in the first quarter of 2026.

On a quarter-on-quarter basis, the economy grew by 0.9%, broadly in line with expectations but below the 1.3% expansion recorded in the previous quarter. For the first half of 2026, economic growth stood at 4.7%, remaining within Beijing’s annual growth forecast range of 4.4% to 4.8%.

China's GDP growth, quarterly (Source: National Bureau of Statistics)

Exports Support Growth, but Domestic Weakness Persists

China’s export sector remained an important source of economic support during the quarter. Resilient overseas demand, including demand for electronics and networking equipment linked to artificial intelligence and data-centre investment, helped maintain industrial activity. Some exporters may also have benefited from businesses bringing forward purchases amid concerns over supply-chain disruptions associated with geopolitical tensions in the Middle East.

However, strong external demand was not sufficient to fully offset continued weakness within the domestic economy. Household spending remained subdued, while business investment and broader capital expenditure showed signs of pressure.

June economic data highlighted this divergence. Industrial production increased by 5.3% year-on-year, exceeding market expectations of 4.7% and accelerating from 4.5% in the previous month. In contrast, fixed-asset investment contracted by 5.7%, extending its decline for a third consecutive month and reflecting ongoing weakness across property, infrastructure and capital spending.

Retail sales increased by just 1.0% in June. Although the result was better than expectations for a modest contraction, consumer spending remained relatively soft, reinforcing concerns over the strength of China’s domestic recovery.

What Does This Mean for Australian Investors?

China’s weaker-than-expected economic growth could have implications for Australian companies with significant exposure to Chinese demand. Mining and commodity stocks may be particularly sensitive if softer investment and property activity weigh on demand for key resources such as iron ore.

However, the continued strength in Chinese industrial production and exports may provide some support to demand for commodities linked to manufacturing, infrastructure, electrification and technology supply chains.

For Australian investors, the latest data presents a mixed picture. China’s export-oriented industries remain resilient, but persistent weakness in domestic consumption, property and investment continues to create uncertainty around the broader economic outlook. Future policy support from Beijing, movements in commodity prices and the pace of recovery in domestic demand are likely to remain important factors for the Australian share market.

Disclaimer: Ace Investors Pty Ltd (ABN 70 637 702 188) authorized representative of MF & CO. ASSET MANAGEMENT PTY LTD (AFSL No.520442). Ace Investors has made all efforts to warrant the reliability and accuracy of the views and recommendations articulated in the reports published on its websites. Ace Investors research is based on the information known to us or which was obtained from various sources which we believed to be reliable and accurate to the best of its knowledge. Ace Investors provides only general financial information through its website, reports and newsletters without considering financial needs or investment objectives of any individual user. We strongly advocate that you seek advice, with your financial planner, advisor or stock broker, the merit of each recommendation before acting on any recommendation for their own specific financial circumstances and realize that not all investments will be suitable for all subscribers. To the scope permitted by law, Ace Investors Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Ace Investors Pty Ltd hereby limits its liability, to the scope permitted by law to resupply of the services. The securities and financial products we study and share information on, in our reports, may have a product disclosure statement or other offer document associated with them. You should obtain a copy of these before making any decision about acquiring any security or product. You can refer to our Financial Services Guide.