China’s manufacturing sector showed signs of slowing in May, highlighting ongoing challenges for the world's second-largest economy and raising important considerations for Australian investors exposed to commodity markets.

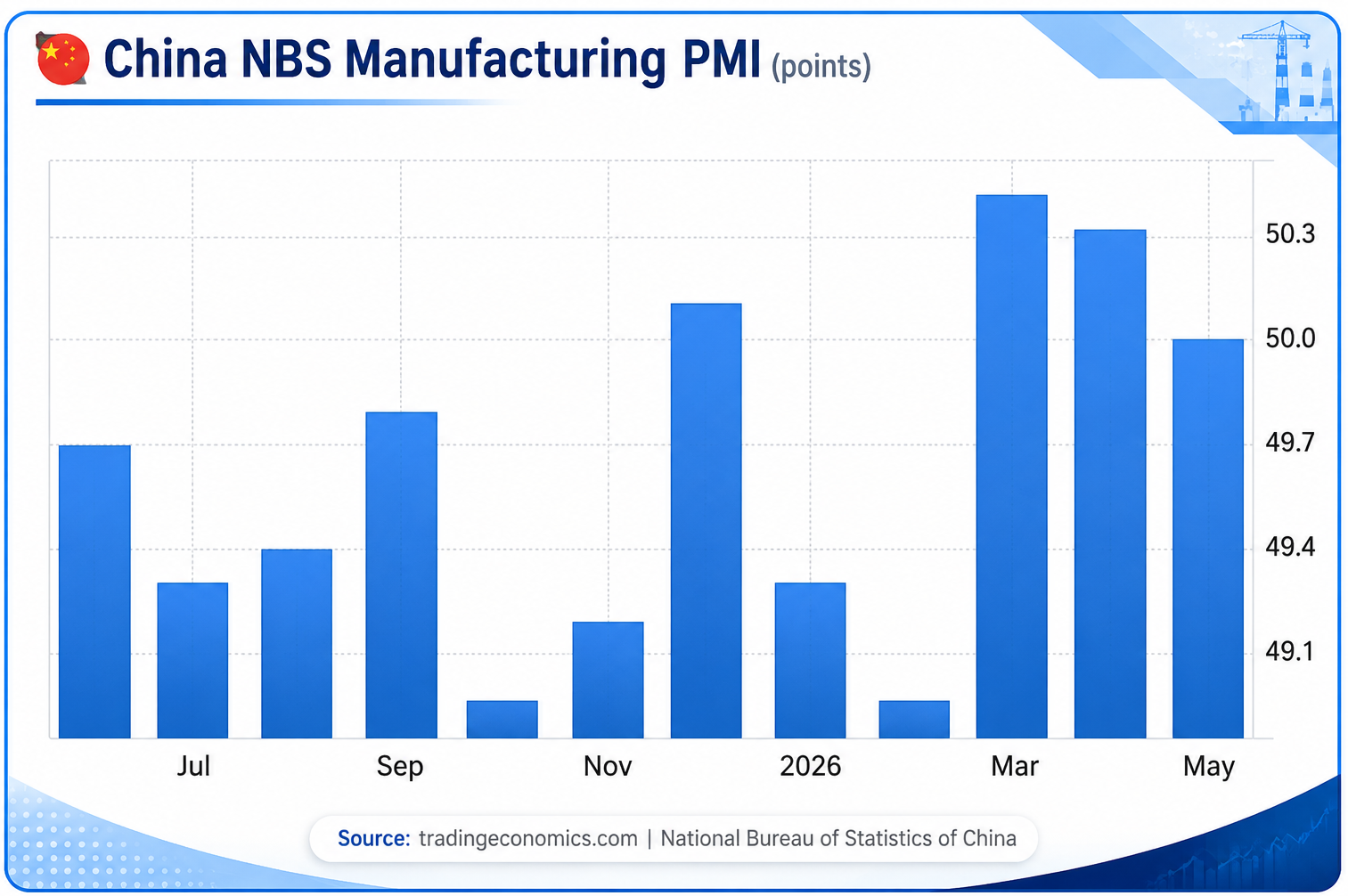

According to official data released by China's National Bureau of Statistics (NBS), the Manufacturing Purchasing Managers' Index (PMI) eased to 50.0 in May from 50.3 in April, matching market expectations. While the reading remains at the threshold separating expansion from contraction, it marks the weakest level in three months and suggests industrial activity is losing momentum.

China’s National Bureau of Statistics Manufacturing PMI (Source: tradingeconomics.com)

The biggest concern came from external demand. New export orders fell sharply to 48.6 from 50.3 in April, slipping back into contraction territory. The decline indicates weaker global demand for Chinese goods, particularly consumer products, which could weigh on manufacturing output in the months ahead.

Cost pressures also remain elevated despite some easing. The raw material purchase price index declined to 60.5 from 63.7 in April but continued to signal rising input costs for manufacturers. Higher energy prices and supply-chain uncertainties have continued to pressure margins, particularly for energy-intensive industries.

Despite the softer headline figure, several sectors demonstrated resilience. High-tech manufacturing and equipment manufacturing recorded PMI readings of 52.9 and 52.1 respectively, reflecting ongoing demand for semiconductors, artificial intelligence-related technologies, and advanced industrial equipment. These sectors continue to benefit from China's long-term push toward higher-value manufacturing.

Meanwhile, China's services sector provided a brighter outlook. The Non-Manufacturing PMI rose to 50.1 from 49.4 in April, exceeding market expectations. Service-sector activity reached a nine-month high, supported by stronger tourism, transportation, telecommunications, and insurance-related activity. The Composite PMI Output Index also improved to 50.5, marking the third consecutive month of expansion in overall economic activity.

For Australian investors, China's economic performance remains particularly significant. As Australia's largest trading partner, China is a major consumer of Australian iron ore, coal, LNG, and other raw materials. Continued weakness in manufacturing and export demand could temper near-term demand for industrial commodities, potentially impacting resource-sector earnings and commodity prices.

However, softer manufacturing data may also increase expectations for additional policy support from Beijing. Any further stimulus measures aimed at boosting domestic demand and economic growth could provide medium-term support for commodity markets and Australian mining companies.

While the recovery in China's services sector is encouraging, the sharp decline in export orders suggests that industrial demand remains under pressure. Investors should continue monitoring Chinese economic indicators closely, as developments in China are likely to remain a key driver of sentiment across Australian resource and equity markets throughout 2026.

Disclaimer: Ace Investors Pty Ltd (ABN 70 637 702 188) authorized representative of MF & CO. ASSET MANAGEMENT PTY LTD (AFSL No.520442). Ace Investors has made all efforts to warrant the reliability and accuracy of the views and recommendations articulated in the reports published on its websites. Ace Investors research is based on the information known to us or which was obtained from various sources which we believed to be reliable and accurate to the best of its knowledge. Ace Investors provides only general financial information through its website, reports and newsletters without considering financial needs or investment objectives of any individual user. We strongly advocate that you seek advice, with your financial planner, advisor or stock broker, the merit of each recommendation before acting on any recommendation for their own specific financial circumstances and realize that not all investments will be suitable for all subscribers. To the scope permitted by law, Ace Investors Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Ace Investors Pty Ltd hereby limits its liability, to the scope permitted by law to resupply of the services. The securities and financial products we study and share information on, in our reports, may have a product disclosure statement or other offer document associated with them. You should obtain a copy of these before making any decision about acquiring any security or product. You can refer to our Financial Services Guide.